Gold has been experiencing a remarkable surge in value in recent years, prompting many investors and analysts to draw comparisons with the explosive rise in gold prices during the 1970s. The historical context of the 1970s—marked by rising inflation, socio-political unrest, and a shift in global monetary policies—appears to offer striking parallels to today’s market. But while the similarities may seem obvious, is the current gold boom really a mirror of the 1970s, or is it something entirely new? In this article, we will explore the key factors driving gold’s rise in both eras, compare the economic and geopolitical conditions, and examine how central banks’ policies today are different from those of the past. Finally, we will analyze what strategic takeaways investors can glean from history.

Deep Dive Into Inflation Parallels Between Eras

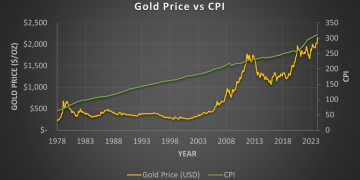

One of the most glaring similarities between the 1970s and today is inflation. In the 1970s, the world faced an unprecedented spike in inflation, driven largely by the oil crisis, geopolitical instability, and the collapse of the Bretton Woods system. Central banks were caught off guard by the inflationary pressure, and traditional monetary policies seemed ineffective in containing rising prices. As a result, investors flocked to gold, driving up its price from around $35 per ounce at the beginning of the decade to more than $850 per ounce by 1980.

Fast forward to the 2020s, and inflation has again become a central concern for economies around the world. The COVID-19 pandemic triggered a global economic shutdown, leading to supply chain disruptions, labor shortages, and record government spending. Governments worldwide have injected trillions of dollars into their economies to stave off economic collapse, contributing to inflationary pressures that resemble those seen in the 1970s. By 2021 and 2022, inflation in the U.S. and Europe was reaching levels not seen in decades, creating an environment where gold once again became an attractive hedge against rising prices.

In both periods, gold has proven to be a reliable store of value in times of inflation. However, today’s inflationary pressures are different in several respects. While the 1970s inflation was driven by oil price shocks and the abandonment of the gold standard, today’s inflation is driven by a combination of supply chain disruptions, labor market imbalances, and unprecedented fiscal and monetary stimulus. Although both inflationary periods are significant, today’s market is navigating a complex set of factors that could result in different outcomes for gold.

Socio-Political Unrest as a Market Driver

The 1970s were a time of profound socio-political upheaval. The Vietnam War was still ongoing, the Watergate scandal in the U.S. shook political confidence, and a series of global crises—including the 1973 oil embargo and the Iranian Revolution—created an atmosphere of uncertainty. This turmoil contributed to the rising demand for gold, as investors sought safe-haven assets in times of political instability.

In the 2020s, we are seeing a new wave of socio-political unrest, albeit with a different flavor. The COVID-19 pandemic triggered global lockdowns, leading to mass protests and social unrest in various parts of the world. Political divisions in the U.S. and Europe have deepened, and there has been a significant shift in the global power structure, with tensions between major economic powers—particularly between the U.S. and China—continuing to rise. Moreover, the war in Ukraine, the global refugee crisis, and the ongoing challenges related to climate change have added new layers of uncertainty to the global landscape.

Despite these differences, the role of gold as a safe-haven asset during times of socio-political unrest remains largely unchanged. Gold tends to perform well when investors lose confidence in government institutions, economic policies, or geopolitical stability. As social unrest and political tensions continue to simmer, the demand for gold as a hedge against instability is likely to persist.

What’s Different About Today’s Central Banks?

Central banks played a pivotal role in the gold market during the 1970s. In 1971, President Richard Nixon’s decision to suspend the convertibility of the U.S. dollar into gold—essentially ending the Bretton Woods system—set the stage for a new era of global currency and monetary policy. The subsequent inflationary environment was, in part, a consequence of this seismic shift in the global monetary system. Central banks, particularly the Federal Reserve, were slow to react to the inflationary pressures that were building in the economy, which allowed inflation to spiral higher and led to a significant rise in gold prices.

Today, central banks are operating in a very different environment. Since the 2008 financial crisis, central banks have implemented a range of unconventional monetary policies, including near-zero interest rates, quantitative easing, and forward guidance. These policies were designed to stimulate economic growth and prevent deflation, but they also contributed to the massive global debt load and rising asset prices. When the COVID-19 pandemic hit, central banks again resorted to massive monetary stimulus, which has led to inflationary pressures not seen since the 1970s.

However, there are key differences in the way central banks are approaching the current economic climate. The Federal Reserve, for instance, has signaled that it is more committed to controlling inflation than it was in the 1970s. In response to rising prices, the Fed has already started raising interest rates and is expected to continue tightening monetary policy in the coming years. The global central banking community is also far more coordinated today, with central banks in Europe, Asia, and other regions taking similar actions to combat inflation. This shift could help avoid some of the runaway inflation seen in the 1970s and could prevent gold from experiencing the same kind of explosive growth seen in that era.

That said, central banks are still highly influential in the gold market. Investors will continue to watch how central banks react to inflation and economic growth, as their decisions will have a significant impact on the future price of gold. The key difference today is that central banks are much more proactive and have a broader range of tools at their disposal to manage economic stability.

Strategic Takeaways from the Past

So, what can investors learn from the gold market of the 1970s as they look toward 2025? There are several important lessons to be drawn from the past.

- Inflation Is a Strong Driver of Gold Prices: The 1970s taught investors that gold is a strong hedge against inflation. If inflation remains elevated in the coming years, gold is likely to remain a valuable asset, even if it does not experience the same dramatic price increases as it did in the 1970s.

- Geopolitical and Socio-Political Instability Increases Gold Demand: The 1970s were a period of significant political unrest, and gold benefitted as a result. Today, we see similar geopolitical tensions and social unrest that could drive further demand for gold, especially in times of crisis.

- Central Banks Are a Key Factor: In the 1970s, central bank policies played a significant role in driving gold prices. Today, while central banks are more proactive in managing inflation, their decisions will continue to have a profound impact on gold prices. Investors should closely monitor central bank actions as they could be a key factor in shaping gold’s future performance.

- Gold’s Role as a Safe-Haven Asset Remains: Despite the differences between the 1970s and today, gold’s role as a store of value during times of economic and political uncertainty remains unchanged. Investors looking to hedge against instability may still find gold to be a reliable choice.

Conclusion

While the rise of gold in 2025 shares certain similarities with the 1970s, such as inflationary pressures and socio-political unrest, the differences are significant. Central banks today are far more proactive in managing inflation, and the global geopolitical environment has evolved in ways that could affect the trajectory of gold prices. However, one thing remains clear: gold’s appeal as a safe-haven asset in times of crisis is as strong as ever. As we move into the 2025, investors would do well to take strategic cues from the past while remaining attuned to the unique dynamics of today’s gold market.

{kind=link}