Detailed Price Analysis of Gold in the Current Market

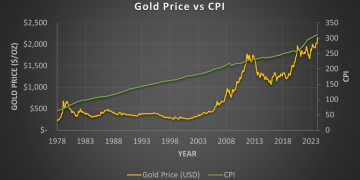

As we advance through 2025, gold remains a cornerstone of financial discussions, drawing attention from seasoned investors, central banks, and individuals seeking wealth protection. Analyzing the current market reveals that gold prices have sustained notable strength, influenced by a combination of lingering inflation concerns, geopolitical uncertainty, and shifts in global monetary policy. As of the first quarter of 2025, gold has fluctuated between $2,000 and $2,200 per ounce, establishing a robust support level that reflects broader economic anxieties.

Recent price movements show that gold continues to be sensitive to real interest rates rather than nominal rates alone. Despite central banks around the world keeping interest rates relatively high to combat inflation, the persistence of inflationary pressures has kept real returns on cash and bonds negative or marginal, sustaining gold’s appeal. Moreover, the dollar index, which inversely affects gold pricing, has exhibited moderate volatility. A slightly weakening dollar throughout late 2024 into early 2025 has provided an additional tailwind for gold prices.

Demand dynamics are equally critical in current price analysis. Central banks, particularly in emerging economies like China, India, and Turkey, have accelerated gold purchases to diversify away from U.S. dollar holdings, citing geopolitical risk and a desire for reserve currency security. Simultaneously, investment demand through gold-backed ETFs has stabilized after two years of outflows, signaling renewed investor confidence. On the supply side, mine production growth has been constrained by rising operational costs, stricter environmental regulations, and logistical challenges, adding a structural supply constraint that supports higher price floors.

Technical indicators further affirm bullish tendencies. The 50-day moving average remains above the 200-day moving average—a classic “golden cross”—pointing to ongoing upward momentum. Furthermore, market positioning data reveals that speculative long positions have increased steadily, though not yet to overheated levels, suggesting that while optimism is present, the market has not entered a speculative bubble phase.

Trends Affecting Gold Prices: Economic Cycles, Geopolitical Events, and Market Speculation

Several interconnected trends are currently driving gold prices and will likely continue to shape the market over the next few years. Economic cycles, particularly the looming potential for a global slowdown or mild recession, heavily influence gold’s trajectory. Although inflation has moderated slightly compared to its 2022–2023 peaks, it remains above the 2% target in most developed economies. This “sticky inflation” dynamic makes central banks cautious about cutting interest rates too aggressively, thereby maintaining uncertainty that benefits gold.

Another critical trend is the enduring impact of geopolitical events. Rising tensions in Eastern Europe, persistent instability in parts of the Middle East, and the increasing assertiveness of China in regional disputes have all elevated gold’s role as a geopolitical hedge. Historically, periods of heightened global tension correlate strongly with gold price surges, as investors seek to shield themselves from unpredictable risks that can disrupt global trade and financial stability.

Currency competition and dedollarization movements are another noteworthy factor. Several emerging economies are exploring alternatives to dollar-dominated trade systems, and this has elevated gold’s profile as a neutral settlement asset. The increase in bilateral trade agreements settled in local currencies, often backed by gold reserves, underscores gold’s expanding role in global financial systems.

In addition, market speculation continues to influence short-term price swings. Algorithmic trading and retail investors, empowered by more accessible trading platforms, have introduced higher volatility into gold markets. While long-term fundamentals remain strong, speculative activities can amplify price movements during news cycles, particularly around central bank policy announcements, inflation data releases, and geopolitical flashpoints.

Environmental, social, and governance (ESG) concerns are also playing an increasingly prominent role. Institutional investors are scrutinizing the environmental impact of gold mining, pushing for greener production methods. Companies that align with ESG standards may command premium valuations, while those that fail to adapt could face operational constraints, indirectly impacting gold supply and supporting higher prices.

Predictions for Future Market Trends Based on Current Conditions

Given the current landscape, future predictions for gold are predominantly bullish, though nuanced by underlying economic shifts. Analysts forecast that gold could reach new all-time highs within the next 12 to 24 months, with consensus estimates suggesting a potential range of $2,300 to $2,500 per ounce if inflation remains above central bank targets and geopolitical risks escalate further.

One primary driver for this forecast is the expected pivot in central bank policies. While aggressive interest rate cuts may not be imminent, gradual easing in late 2025 or early 2026 is anticipated as economies slow and inflation targets remain elusive. Lower real interest rates would enhance gold’s attractiveness compared to income-generating assets like bonds, drawing more institutional and retail flows into the gold market.

Another significant trend is the continued expansion of gold’s role in central bank reserves. If dedollarization accelerates, more countries may bolster their gold holdings as a way to assert monetary sovereignty. This structural demand shift would create a persistent underpinning for gold prices, regardless of cyclical investment demand.

Consumer demand from Asia is also poised to support the market. As economic growth resumes in China and India, pent-up demand for gold jewelry, bars, and coins is expected to drive significant physical gold consumption. Seasonal buying patterns—particularly during cultural festivals and weddings—could add cyclical upward pressure to prices, particularly in the latter half of 2025.

Technological innovations in the gold market are another area to watch. The rise of tokenized gold assets—digital representations of physical gold secured on blockchain platforms—may attract younger, tech-savvy investors who value both the stability of gold and the convenience of digital assets. This could expand gold’s investor base, increasing market liquidity and supporting higher prices.

However, it is important to acknowledge potential headwinds. A sharp economic recovery stronger than anticipated could dampen gold’s appeal if risk appetite returns aggressively to equities and risk assets. Similarly, a rapid stabilization of geopolitical tensions, while desirable globally, could reduce safe-haven demand. That said, historical precedent suggests that gold’s role as a wealth preservation tool remains resilient even during periods of relative calm, albeit with lower price volatility.

Long-term investors would be wise to view gold not simply as a speculative asset but as a strategic portfolio component that offers diversification benefits, inflation protection, and crisis insurance. Based on current conditions and historical patterns, allocating a portion of assets to gold—whether through bullion, ETFs, mining stocks, or physical jewelry—appears prudent in an increasingly complex and uncertain global environment.

In summary, analyzing current gold price trends against the backdrop of economic cycles, geopolitical shifts, and market behavior suggests a favorable future for gold investors. While volatility is inevitable, the structural forces supporting gold prices today are likely to persist, offering both stability and opportunity for those who strategically position their portfolios.

{kind=link}