Gold’s Role as a Safe Haven in Economic Downturns

Throughout history, gold has held a unique status as a safe haven asset during periods of economic turmoil. Whether it’s a financial crash, sovereign debt crisis, or global recession, gold has typically performed a stabilizing function within investment portfolios. Its intrinsic value, lack of counterparty risk, and global recognition make it an attractive refuge when other asset classes are under pressure. During recessions, investors often flee from volatile equities, depreciating currencies, and weakening bonds, turning instead to gold for its perceived security. Gold’s behavior during past downturns provides a wealth of insight for modern investors aiming to craft recession-proof strategies. Understanding these historical patterns can guide decisions in an uncertain future.

The Great Depression: Gold as a Monetary Anchor

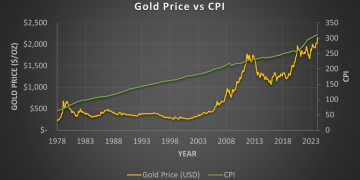

The Great Depression of the 1930s stands as one of the most severe economic collapses in modern history. During this period, gold served less as an investment asset and more as a fundamental part of the global monetary system under the Gold Standard. As economies contracted and banks failed, the value of gold remained remarkably stable because currencies themselves were pegged to gold. The U.S. government even revalued gold upward in 1934, raising the official price from $20.67 to $35 per ounce to combat deflation and stimulate the economy. This act both confirmed gold’s essential role and demonstrated how governments themselves turned to gold in times of crisis. For investors today, the Great Depression underlines gold’s historical resilience not merely as a tradable asset but as a core element of financial systems under stress.

The 1970s Stagflation: Gold’s Ascent in Inflationary Recessions

The 1970s brought a new type of economic pain: stagflation—a toxic mix of stagnant growth and rampant inflation. Unlike the 1930s, the U.S. was no longer on the Gold Standard, having decoupled in 1971. With the dollar now a fiat currency, gold prices were free to fluctuate based on market forces. The results were dramatic. As inflation soared and economic growth stalled, gold prices exploded from around $35 an ounce in 1971 to over $800 by 1980. Investors fled fiat currencies that were rapidly losing purchasing power, seeking protection in tangible assets like gold. This episode reinforces an important lesson: gold’s ability to preserve value is particularly potent during periods when inflation and recession combine. Modern investors facing inflationary threats may find gold an even more critical portfolio component.

The Early 2000s Recession: A Quiet but Steady Climb

Following the dot-com bubble burst in 2000, the U.S. economy entered a mild recession. Gold’s behavior during this period was less dramatic than in the 1970s but equally telling. While equities plunged and technology stocks collapsed, gold quietly began a multi-year bull market. From a low of around $250 an ounce in 2001, gold steadily rose, reaching $400 by 2004. Investor anxiety over corporate scandals (like Enron), geopolitical tensions (such as 9/11 and the Iraq War), and easy monetary policy all contributed to gold’s steady accumulation. This period highlighted that gold doesn’t necessarily require explosive crises to perform well—it can thrive during broader market skepticism and policy-driven liquidity expansions. For current investors, this suggests that even in modest recessions, gold can act as a quietly compounding asset rather than just a crisis hedge.

The 2008 Financial Crisis: Gold’s Ultimate Stress Test

The 2008 financial crisis was perhaps the most significant stress test for gold in the modern era. During the initial stages of the crisis, gold prices fell alongside equities as investors liquidated assets to raise cash. However, this decline was short-lived. By late 2008, gold began rebounding sharply, surging from around $700 an ounce to over $1,200 within two years. Massive central bank interventions, including quantitative easing and near-zero interest rates, debased fiat currencies and increased gold’s appeal. The 2008 experience offers a crucial lesson: while gold may experience short-term volatility during liquidity crunches, its role as a safe haven tends to reassert itself strongly as financial systems stabilize. Investors today should anticipate potential short-term shocks but recognize the medium-term resilience gold typically exhibits in major downturns.

The COVID-19 Recession: Gold in a Pandemic Economy

The COVID-19 pandemic triggered one of the fastest global recessions on record in early 2020. Like 2008, gold initially dipped during the liquidity scramble but quickly rebounded, reaching an all-time high above $2,000 an ounce by August 2020. Unprecedented monetary stimulus, fiscal expansion, and fears over currency debasement propelled gold higher. Yet, unlike past recessions, gold’s rally was tempered by the rapid recovery in equity markets, particularly in tech stocks. Still, gold’s strong performance amid the pandemic underscores its enduring relevance as a hedge against systemic shocks and monetary excess. For today’s investors, the COVID-19 case suggests that gold remains an essential component for managing both unexpected and systemic risks, even in environments where recovery narratives are strong.

Comparing Historical Patterns: Key Takeaways for Today

Across all major recessions, several key patterns emerge regarding gold’s behavior. First, gold typically benefits from environments of fear, uncertainty, and liquidity injections. Second, while gold can experience short-term declines during initial market shocks, its medium- and long-term resilience is robust. Third, the drivers of gold’s strength vary: inflation, monetary expansion, geopolitical instability, and financial system distrust all play critical roles. These lessons imply that gold’s historical performance is not tied to a single economic outcome but rather to a broad spectrum of instability factors. For today’s portfolios, this highlights the importance of considering gold not merely as an inflation hedge or dollar hedge but as a multi-dimensional insurance asset.

Applying Historical Lessons to Modern Investment Strategies

Modern investors can use these historical insights to build more resilient portfolios. First, maintaining a strategic allocation to gold—typically 5% to 15% depending on risk appetite—can provide downside protection without overexposing the portfolio to non-yielding assets. Second, gold should be viewed with a medium- to long-term horizon; short-term price volatility is normal but does not diminish gold’s ultimate safe haven role. Third, diversification within gold-related assets—such as combining physical gold, ETFs, and select mining equities—can enhance returns while spreading risk. Investors should also monitor macroeconomic indicators closely: surges in money supply, rising inflation expectations, weakening currencies, and geopolitical tensions are all traditional bullish signals for gold. Finally, understanding gold’s behavior relative to real interest rates is crucial. Historically, gold thrives when real interest rates (nominal rates minus inflation) are negative or declining. Watching these trends can provide actionable signals for adjusting gold exposure.

Conclusion

The historical record is clear: gold has demonstrated remarkable resilience across a wide range of economic downturns, from the deflationary collapse of the Great Depression to the inflationary chaos of the 1970s and the systemic financial crises of the 21st century. Each period offers unique insights, but the overarching theme remains consistent—gold acts as a reliable store of value when traditional financial assets falter. As the global economy faces an uncertain future characterized by potential inflation, monetary policy shifts, and geopolitical risks, investors can draw on history to inform smarter portfolio strategies. Incorporating gold thoughtfully, maintaining realistic expectations, and staying alert to macroeconomic triggers can help investors not only survive but potentially thrive in the next recessionary environment.

{kind=link}