Introduction: Gold’s Persistent Dominance

Among the spectrum of precious metals, gold has historically held a unique status. Unlike its metallic cousins—silver, platinum, and palladium—gold combines the attributes of a commodity, a monetary asset, and a psychological anchor for investors during uncertainty. While all four metals are often grouped together, their market dynamics are distinct. Recent price trends reveal that gold is not just holding its ground but actively outpacing its peers. Understanding why gold is outperforming other precious metals requires examining both quantitative price movements and the deeper undercurrents of safe-haven demand, industrial usage, and investment psychology.

Gold vs Silver: The Battle of the Traditional Pair

Gold and silver have shared a long financial history, often moving in tandem due to their roles as monetary metals. However, their recent price trajectories tell a different story. Over the past two years, gold has reached repeated all-time highs, while silver has struggled to break convincingly above $30 per ounce. The gold-to-silver ratio—a measure of how many ounces of silver it takes to buy one ounce of gold—has widened significantly, often exceeding 80:1, far above the historical average of around 50:1.

Several factors explain this divergence. First, silver is far more tied to industrial demand than gold, with uses ranging from solar panels to electronics. While industrial demand is growing, it also subjects silver to the volatility of global economic cycles. In contrast, gold’s value is driven predominantly by investment and central bank purchases, making it less susceptible to the vagaries of industrial production.

Additionally, silver’s smaller market size makes it more volatile. Although this can lead to outsized gains during bull markets, it also results in sharper declines during risk-off periods. Investors seeking safety during uncertain times have consistently favored gold over silver, reinforcing gold’s role as the ultimate safe haven.

Platinum and Palladium: Industrial Metals Struggle

Platinum and palladium occupy yet another niche within the precious metals complex. Their primary demand drivers are industrial, particularly in the automotive sector for catalytic converters. However, structural shifts in global industries have weakened their appeal relative to gold.

Palladium enjoyed a spectacular bull market from 2016 to 2021, driven by tightening emissions standards that increased demand for gasoline-engine catalytic converters. However, as electric vehicle adoption accelerates, palladium’s dominance in the automotive sector faces an existential threat. Furthermore, substitution pressures are mounting, with automakers looking for cheaper alternatives like platinum as palladium prices soared.

Platinum, for its part, has seen periods of optimism, especially with hydrogen fuel cell development, but broader industrial weaknesses and supply issues in South Africa have made its recovery uneven at best.

Neither platinum nor palladium enjoys the deep monetary or psychological appeal that gold commands. During market crises, investors do not instinctively flock to platinum or palladium. They seek gold, reinforcing its primacy when uncertainty reigns.

What Price Trends Reveal About Safe-Haven Preferences

Safe-haven assets are valued not just for their scarcity but for their perceived ability to hold value when everything else falters. Gold’s resilience compared to silver, platinum, and palladium highlights how market participants distinguish between metals when allocating assets during periods of fear or volatility.

When geopolitical tensions escalate, inflation fears mount, or financial markets tremble, gold consistently receives inflows, as evidenced by surging gold ETF holdings and robust physical demand from central banks and high-net-worth individuals. Meanwhile, silver, platinum, and palladium often behave more like industrial commodities, falling victim to growth concerns and inventory liquidation.

In effect, gold has become a barometer for global anxiety. The more uncertain the macroeconomic outlook, the higher the premium investors are willing to pay for gold’s perceived security. This trend has been further reinforced by central banks increasingly stockpiling gold as a hedge against currency devaluation and systemic financial risks.

The Monetary Role of Gold vs Industrial Metals

A fundamental reason why gold is outpacing other precious metals lies in its dual nature as both a commodity and a form of money. Unlike silver, platinum, and palladium, which derive a substantial portion of their value from industrial use, gold’s demand profile skews heavily toward investment and wealth preservation.

Central banks buy gold as a strategic reserve, but they do not buy platinum or palladium. Sovereign wealth funds and long-term institutional investors allocate to gold for diversification, but seldom touch other precious metals unless as part of speculative plays. Even retail investors buying coins and bars overwhelmingly favor gold over alternatives.

The emergence of digital gold platforms and the growth of gold-backed financial products such as ETFs have made it even easier for investors to access gold, amplifying its liquidity and attractiveness relative to other metals.

This monetary function insulates gold from the cyclical nature of industrial demand. When global manufacturing slows, platinum and palladium prices typically decline. Gold, in contrast, often rallies as investors seek sanctuary from falling asset prices and declining economic prospects.

Inflation, Interest Rates, and the Gold Premium

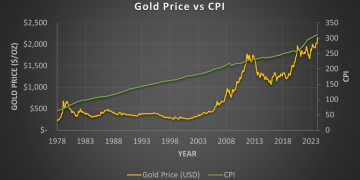

One of the defining features of the current macroeconomic environment is stubborn inflation coupled with high nominal interest rates. Historically, rising rates are seen as a headwind for gold because they increase the opportunity cost of holding a non-yielding asset. Yet in the current cycle, gold has managed to thrive despite elevated rates.

This anomaly can be explained by the persistence of negative real rates—where inflation-adjusted returns on bonds remain poor—driving investors toward gold as a store of real purchasing power. Silver, platinum, and palladium, lacking strong monetary characteristics, do not offer the same hedge against real rate erosion.

In this context, the investment premium attached to gold has grown sharply. Investors are not simply buying gold because of fear or speculation; they are buying it as a rational response to structural shifts in monetary policy, inflation expectations, and geopolitical fragmentation.

Supply-Side Dynamics

Supply dynamics also play a role in gold’s outperformance. While new gold production remains relatively stable, discovery rates of large, high-grade gold deposits have declined dramatically over the past two decades. Meanwhile, the costs of gold mining have steadily increased due to regulatory, environmental, and energy challenges.

In comparison, silver production is often tied to base metals like copper and lead, meaning its supply is less responsive to price signals. Platinum and palladium production is concentrated in politically and economically unstable regions, such as South Africa and Russia, creating risks of supply shocks but also contributing to long-term uncertainty and investment hesitancy.

Gold’s supply profile—steady but tightening over time—supports a secular bull case, especially as demand remains robust from multiple fronts.

Technological Innovations and Their Limited Impact on Gold

Technological innovation has a profound impact on industrial metals. New battery chemistries can alter the demand for palladium. Advances in green hydrogen could eventually boost platinum consumption. Silver’s role in solar panels and electronics may grow with technology, but it also faces competition from alternative materials.

Gold, however, stands largely outside this dynamic. Its value proposition is not tied to technological shifts but to timeless fundamentals: scarcity, durability, universality, and liquidity. As such, technological disruption, which could upend the outlook for other metals, has minimal impact on gold’s core appeal.

Investment Strategy: Allocating Among Precious Metals

Given the current environment, investors should think carefully about how they allocate among precious metals. Gold should remain the cornerstone of any precious metals portfolio, offering stability and serving as a hedge against systemic risks. Silver can be seen as a leveraged play on gold, suitable for more aggressive investors willing to tolerate higher volatility.

Platinum and palladium, while offering upside potential tied to industrial and technological trends, should be treated as speculative positions rather than core holdings. Their prices are more susceptible to economic downturns and sector-specific shocks.

A prudent allocation strategy might involve a 70-20-10 split between gold, silver, and platinum/palladium, adjusted based on individual risk tolerance and macroeconomic outlook.

Conclusion: Gold’s Enduring Appeal

In the race among precious metals, gold’s current outperformance is not a temporary phenomenon but the result of deep, structural advantages. Its monetary status, robust safe-haven demand, insulation from industrial cycles, and supply dynamics have propelled it ahead of silver, platinum, and palladium.

As global uncertainties persist—from inflationary pressures and geopolitical risks to financial market volatility—gold’s unique attributes are likely to remain in high demand. For investors seeking a resilient asset in an unpredictable world, gold continues to shine brighter than its metallic peers, offering both security and strategic advantage in a rapidly evolving financial landscape.

{kind=link}